Bio

I work on optimization and networks at Autonomous Mobility & Delivery team of Uber. Previously, I was a postdoctoral research scientist at Columbia IEOR and Data Science Institute, hosted by Agostino Capponi. In 2024, I received PhD in MS&E with PhD Minor in Statistics from Stanford. I was fortunate to be advised by Markus Pelger as a member of the Advanced Financial Technologies Lab.

Doctoral dissertation committee: Markus Pelger, Kay Giesecke, Itai Ashlagi, Han Hong, Jann Spiess.

Contact: jiachengzou [at] alumni.stanford.edu

Research brief

I develop statistical methods for inference in large dimensional time series data to make better decisions. My goal is to design useful tools merging econometrics and Transformer-based ML.

My current work includes graph neural networks applications in supply chains and learning in non-stationary environment.

See more in my research tab.

Updates

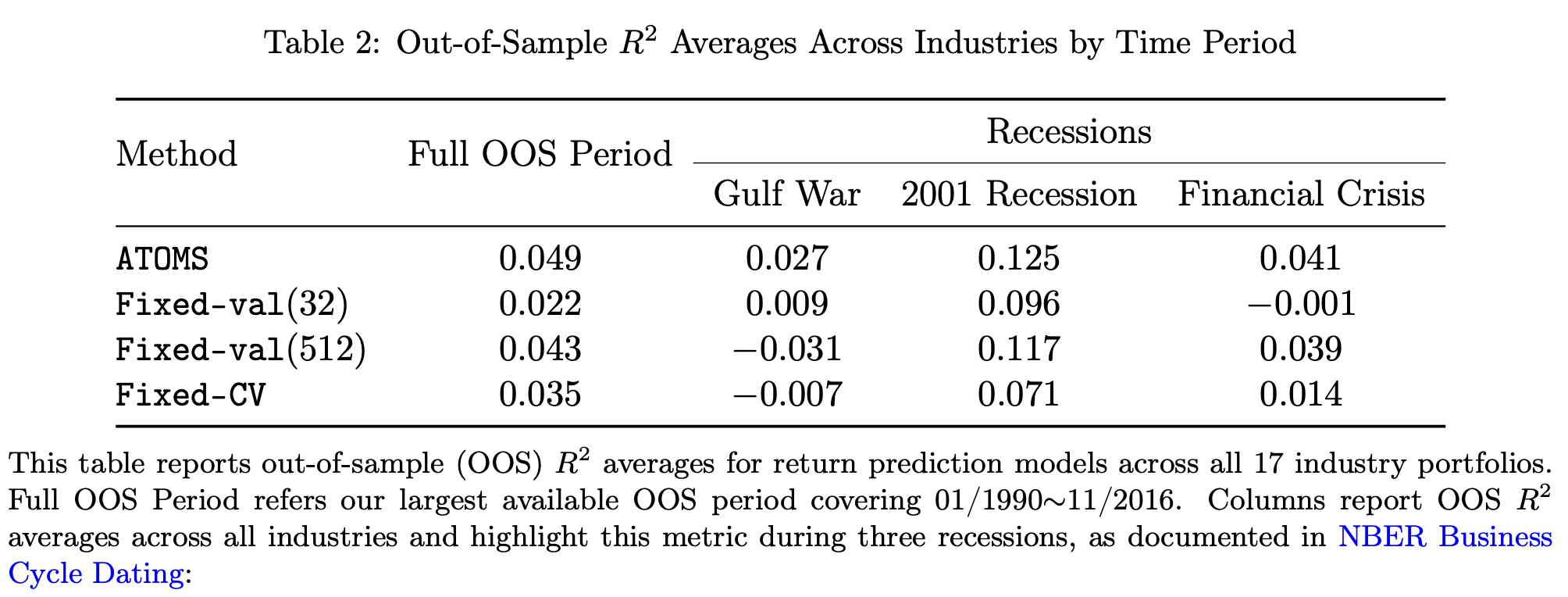

[Dec 2025] New paper the Nonstationarity-Complexity Tradeoff in Return Prediction is now posted. Our method ATOMS leads to better performance during non-stationarity e.g. recessions:

[Dec 2025] R&R at Journal of Financial Economics (JFE) for our graph learning for supply chain paper.

[Apr 2025] R&R at Management Science (MS) for our panel inference paper.

[Aug 2024] Present panel inference in Frontiers of Economics and AI+ML Meeting at Cornell.